State of Climate Transitions

A 2024 Guide for Companies and Investors in the Land Economy

The forest, land and agriculture sectors (FLAG) are particularly vulnerable to physical climate risks as rising temperatures and changing weather patterns threaten crop yields, livestock health and much more. These sectors are also a major contributor to climate change, emitting 23 percent of global greenhouse gas emissions. But, with the potential of land to store carbon, these sectors could offer up to 20 percent of the actions needed globally to mitigate the worst impacts of climate change by 2050. This opens up companies and investors in these sectors to significant risks and opportunities as the economy transitions to a low carbon future.

What are Climate Transitions?

Climate change and the actions taken to mitigate its impacts, known as climate transitions, represent some of the largest systemic changes our economies have ever seen. ‘Climate transitions’ refer to shifts in domestic policy, consumer preference, international regulations, competition driven by technology and other market demands for sustainability that will transform the future of the global economy. Climate transition risks – legal and policy, technology, market and reputation – are all potential pitfalls that can impact performance and are increasingly critical to address, and they all present corresponding opportunities for market leaders.

Legal and policy trends

Policy, regulations and legal rulings from an increasing number of countries and regions now require the private sector to disclose, certify and develop a pathway to reduce emissions from their operations, supply chains and investment portfolios.

Technology trends

Technology, from innovations in reducing livestock methane emissions and advanced agricultural technology to climate smart agriculture in deforestation hot spots, is offering higher efficiency and more resilient alternatives for businesses in the land economy.

Market trends

Frontrunner companies and investors are proactively reducing their exposure to high-emissions intensity activities in favor of sustainable alternatives.

Reputational trends

Reputational concerns around environmental degradation and deforestation, from activist shareholders to concerned consumers, are increasing the pressures businesses face from their stakeholders.

What activities create the most emissions?

FLAG sectors are cumulatively responsible for nearly 22 percent of annual greenhouse gas emissions, with some agricultural activities driving the lion’s share of emissions. Companies and their investors exposed to unsustainable agricultural practices face the most significant climate transitions as high emitters are increasingly scrutinized.

Explore how high-emission activities translate to climate risks and opportunities

Global views: Threats vary by region

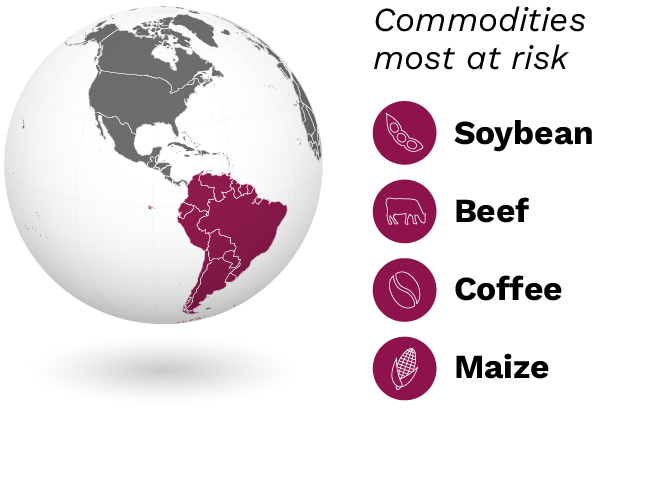

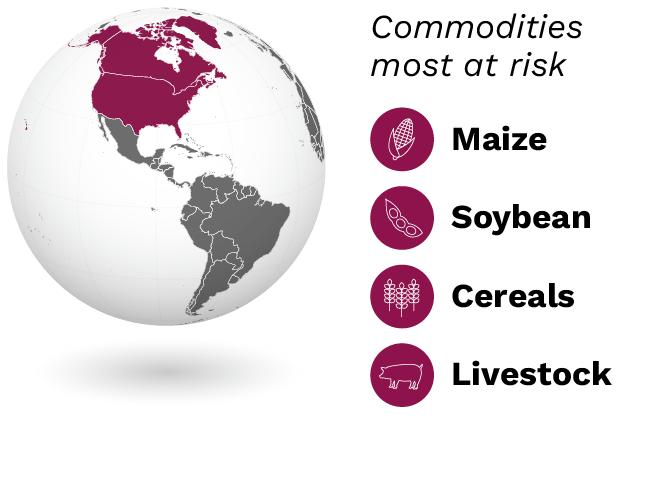

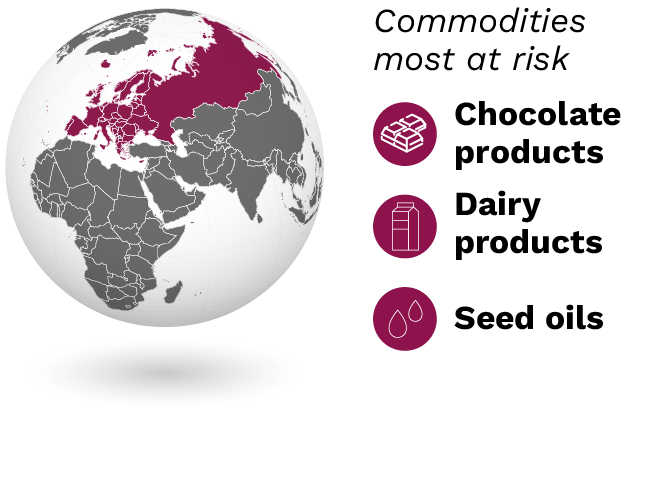

Those involved in the trade of at-risk commodities, and regions with a higher production of these, may face near-term threats due to links to deforestation, high-emission intensity and expansive land use practices, and a resulting lack of certification and loss of market access. For example, South America is highly exposed to commodities linked to deforestation including soybean, beef, coffee, maize and sugarcane, and in Europe, downstream companies are exposed to risks from commodities including chocolate products, dairy products and seed oils due to shifting consumer preferences and growing regulatory restrictions.

However, these threats present opportunities for companies and investors to secure future financial stability by reducing transition risks, and thus, weighted average cost of capital, through exploring emerging markets and diversified revenue streams, adopting developing agricultural technologies and reducing emissions.

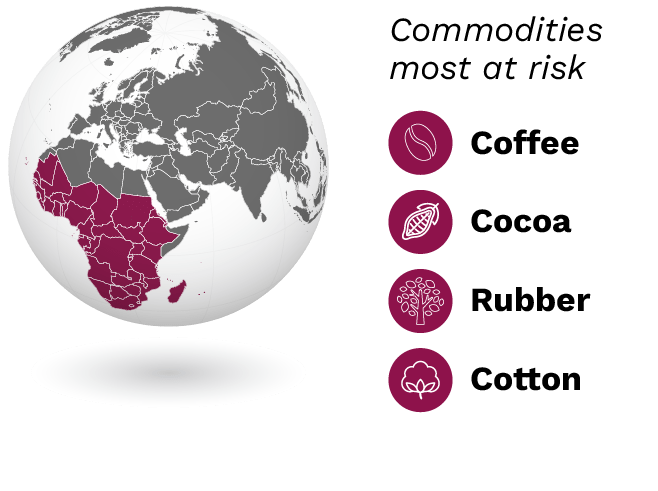

Sub-Saharan Africa

High exposure to deforestation-prone commodities coupled with preexisting infrastructure issues leaves FLAG sectors open to significant climate-related transition risks.

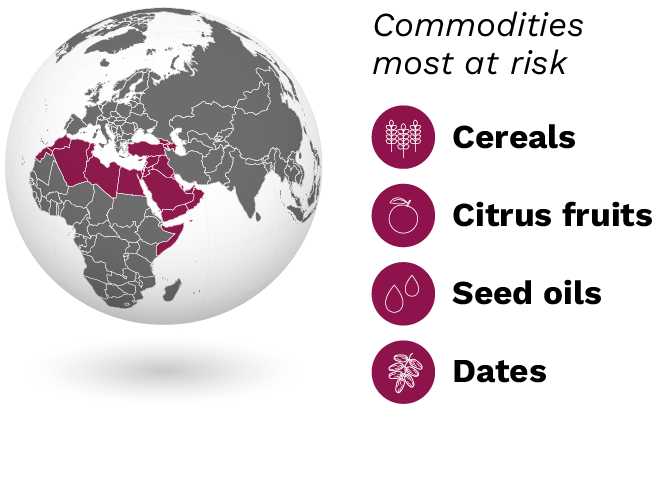

High exposure to deforestation-prone commodities coupled with preexisting infrastructure issues leaves FLAG sectors open to significant climate-related transition risks.Middle East and North Africa

Increased risk from physical climate events may result in more aggressive responses from government organizations aiming to stem further loss of arable land.

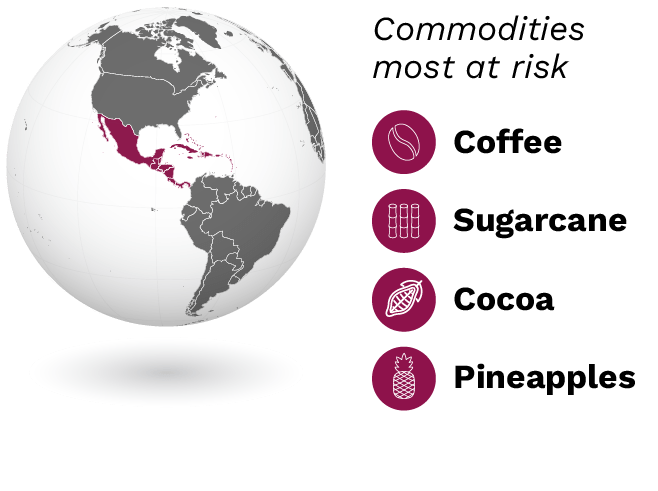

Increased risk from physical climate events may result in more aggressive responses from government organizations aiming to stem further loss of arable land.Central America and the Caribbean

Reliance on high emission farming methods for coffee, sugarcane and cocoa production threatens market access.

Reliance on high emission farming methods for coffee, sugarcane and cocoa production threatens market access. South America

South America is highly exposed to deforestation-linked commodities.

South America is highly exposed to deforestation-linked commodities.South America

South America is highly exposed to deforestation-linked commodities.North America

North America faces transition risks throughout FLAG value chains.

North America faces transition risks throughout FLAG value chains. Europe

Europe’s FLAG sector climate transitions materialize primarily in end-stage processing.

Europe’s FLAG sector climate transitions materialize primarily in end-stage processing.South and Central Asia

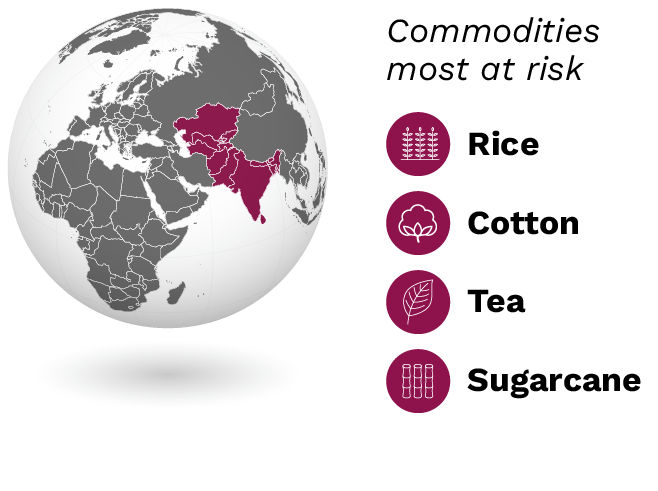

South and Central Asia lead the world in rice cultivation—a process responsible for significant methane emissions.

South and Central Asia lead the world in rice cultivation—a process responsible for significant methane emissions. East/Southeast Asia and Oceania

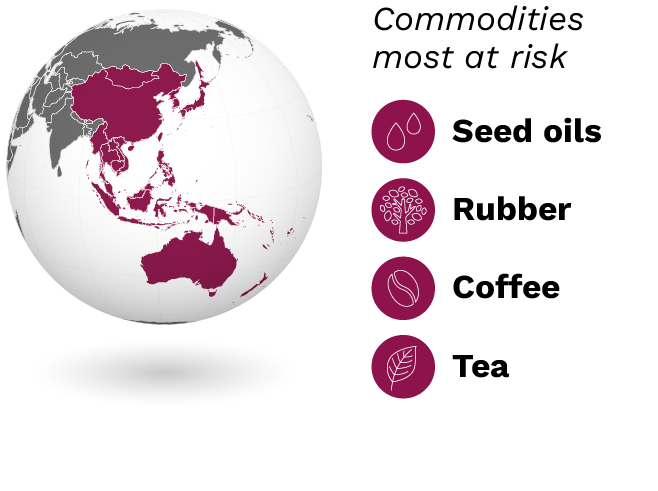

Leading businesses and investors exposed to deforestation-linked commodities such as palm oil, rubber and coffee have faced intense public scrutiny.

Leading businesses and investors exposed to deforestation-linked commodities such as palm oil, rubber and coffee have faced intense public scrutiny.Read more about regional and global impacts on the land economy.

Legal and policy trends

Governments, regulators and policymakers around the globe are increasingly recognizing the severity of climate change impacts and are beginning to demand disclosure and certification. As climate incentives, emissions costs, trade restrictions and disclosure regulations accelerate, emission intensive companies and their investors are at risk of increased operating costs, reduced market access and supply chain disruptions compared to competitors that take early action to mitigate climate risks.

Three legal and policy trends

Increasing climate-related financial disclosure requirements are forcing public disclosure of the financial impacts of climate change, informing investment decisions and shining a light on emission intensive companies with higher climate risks. 35 regions and nations have now adopted laws mandating climate-related financial disclosures. Disclosure frameworks include the Task Force on Climate-Related Financial Disclosures (TCFD), Carbon Disclosure Project (CDP), Global Reporting Initiative (GRI), International Sustainability Standards Board (ISSB) and European Sustainability Reporting Standards (ESRS).

Growing supply chain due diligence and sustainability certification requirements are limiting market access to products exposed to deforestation or other environmental degradation. For example, the European Union deforestation regulation to limit EU consumption of products linked to deforestation or forest degradation restricts key commodities linked to deforestation without certifications.

Increasing government commitments to net zero emissions will accelerate incentives for the adoption of sustainable practices and carbon taxes, market restrictions and fines for environmental degradation, amplifying competitive advantages for low emission and deforestation free products. Since the 2015 Paris Agreement, national governments have collectively pledged 92 percent of the global economy to a net-zero emissions target.

Technology trends

Climate-smart solutions and growing access to advanced agricultural technologies are helping producers meet the challenges of climate change while unlocking opportunities for growth. Companies that take early action to adopt agricultural technology and climate smart practices that improve efficiency, reduce land use requirements and lower emissions can benefit from more resilient demand, lower costs and better access to financing.

Three technology trends

Investments in research and development are driving advancements in climate-smart agriculture (CSA) that are enhancing resilience, enabling climate mitigation, improving productivity, lower operating costs and favorable positioning against peers. For example, The Brazilian Agricultural Research Corporation (Embrapa) has led the development and promotion of integrated crop–livestock–forestry, silvopasture and other agroforestry strategies, and the Bill & Melinda Gates Foundation has committed USD 1.4 billion to help meet the climate adaptation needs of smallholder farmers.

Rapidly developing agricultural technology is driving efficiency and creating market leaders by allowing farmers to optimize their operations, reduce waste and lower their carbon footprint. For example, combinations of innovations including precision agriculture, farm automation and robotics are estimated to reduce 71 percent of the emissions from row crops.

Emerging solutions for reducing livestock methane emissions are providing companies and their investors with opportunities to mitigate the impact of carbon tax policies and other emissions-related costs, while reducing substitution risk from low emission alternatives. For example, feed additives and fat supplements for cattle can cut cattle methane emissions by 10 to 40 percent, while natural solutions such as seaweed can cut these emissions by up to 80 percent. Other solutions include pasture-based rotational grazing and the breeding of larger, healthier cattle.

Market trends

Globally, markets are rapidly evolving in the face of climate change and companies and investors are seeking opportunities to diversify their revenue and achieve sustainable differentiation. Companies and investors that lean into new market opportunities and adopt low emission, sustainable production practices can capture growing consumer demand and higher revenue under climate transitions, while competitors face disruptive risks to traditional business models.

Five market trends

Diversification into emerging alternative markets, including in dairy alternatives, plant-based proteins and other low-carbon goods, are providing companies and investors increased resiliency in the face of climate transitions in a market that increasingly values product sustainability. Dairy and meat alternatives markets are expected to grow 30 and 36 percent, respectively, over the next decade.

Growing consumer preferences for sustainable goods is rewarding emission reduction practices, and companies and their investors who fail to integrate emissions reductions and monitoring along their supply chains may lose their competitive advantage. For example, sustainable products achieved a more than a 35 percent higher five-year growth rate compared to their conventional counterparts.

Downstream companies are increasingly mandating sustainability commitments from their suppliers to mitigate the reputational risk associated with deforestation, which limits market access for deforestation-linked suppliers. For example, 60 percent of 350 FLAG sector companies most exposed to palm oil, soy, beef, leather, timber, pulp and paper now have no-deforestation policies, and actions by companies such as Unilever, Proctor & Gamble and Nike are leaving non-compliant producers with limited avenues.

Loans and investment policies are increasingly conditional on sustainable practices including climate-smart techniques and reductions in emission intensity. High emission companies are seen as riskier than lower emission competitors, which leads to differences in the weighted average cost of capital. Strict standards for borrowers from public lenders such as the European Investment bank, the World Bank and the International Fund for Agricultural Development and commercial lenders such as Rabobank, are aiding the adoption of sustainable practices.

Carbon markets and nascent biodiversity markets are offering revenue diversification opportunities, and are expected to grow to around USD 250 billion and USD 69 billion respectively by 2050. Nature-based solutions may present a more reliable future for low margin producers and include afforestation and deforestation, clean energy initiatives, carbon sequestration, forest and nature conservation and restoration.

Reputational trends

Heightened public awareness of climate change and scrutiny are driving more transparency and climate action, as companies and investors seek to avoid reputational damage from being linked to environmental degradation or deforestation. Increased transparency, through advanced satellite monitoring, ever faster information dissemination, disclosure requirements and shareholder advocacy, is creating a growing divide between climate leaders and laggards and amplifying the financial impact of reputational risks and opportunities.

Four reputational trends

Shareholder activism is driving sustainable business practices, including zero-deforestation policies for leading traders such as Wilmar International, Bunge and Archer Daniel Mills, and greenhouse gas reduction goals for downstream giants, Tyson Foods and Unilever. Shareholder resolutions, external public campaigns and dialogue with company executives will continue to drive the adoption of climate commitments as investors see emission intensive companies as inherently more risky under climate transitions.

Growing scrutiny and access to monitoring technologies are driving pressure on companies and investors to accurately report on, and meet, climate commitments, or risk reputational damage and regulatory scrutiny. Almost 60 percent of the world’s largest publicly traded companies committed to net zero emissions by at least 2070. Sustainability leaders in the FLAG sector include Unilever, Danone and Nestle.

Tech-enabled advancements like satellite monitoring along supply chains, are amplifying the reputational risks faced by companies and investors that fail to adopt deforestation-free and low emission practices, risking brand damage and divestment. Companies such as Unilever and Danone are leading through proactive reporting, updates and mandates from their supply chains, with Unilever’s Sustainable Living brands accounting for 75 percent of the company’s growth in 2020.

The rapid spread of information and rising internet access globally, around 7.9 billion people by 2029, are amplifying negative and positive brand value impacts, with 30 percent of a company’s market value impacted by reputational events. Companies that disclose environmental impacts and adopt rigorous actions to mitigate climate risks will strengthen their brand resilience, and those that fail to risk both reputational and financial damage.

How Climate Transitions Risks Show up on the books

The climate transition risks facing the land sector can be categorized broadly into four categories, legal and policy risks, technology risks, market risks, and reputation risks. The following examples are a guide to help stakeholders understand how climate transitions translate into real-life impacts on company Income Statements and Balance Sheets.

Market risks

Legal and policy risks

Technology risks

Reputational risks

Read more about climate transition risks

What can companies and investors do to mitigate financial risk?

Go deeper on the recommendations and potential benefits.

Want to learn more?

Sign up for our latest news, thoughts, and insights.

Copyright © Orbitas 2026